PARTNER PRO VAŠI LAKOVNU

Prodejna

Měsíční akce

BORI lazura - gelová konzistence

NOVINKA

- vysoce tixotropní lazura

- nátěr vhodný pro stropní a výškové konstrukce, např. podbití u domů - lazura nestéká

- při převržení plechovky, obsah zůstává

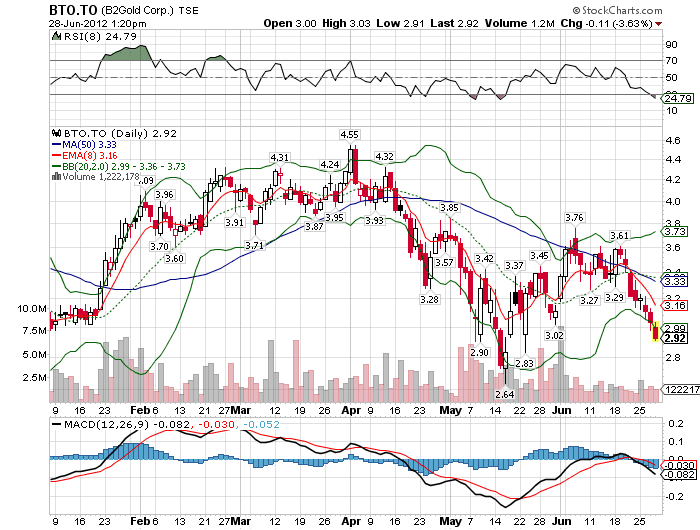

variable cost

Fixed Cost, also called ‘overhead cost’ or ‘indirect cost’ is the business expenditure that does not get affected by the increased or decreased production or sale of goods and services. This business expense remains the same for an entire financial period and is time-dependent. A fixed cost is an expense that does not change as production volume increases or decreases within a relevant range.

- Over- or under-absorbed overhead costs are closed and transferred to the cost of goods sold account.

- It is added to the cost of the final product along with the direct material and direct labor costs.

- In a certain factory, three products are made from different materials by similar processes.

If you purchase electricity from the outside, you can easily know the total charge of power consumption. Factory costs include material costs, labor costs, and proportional costs of factory costs. You can also charge different departments for repair and maintenance equipment, depending on the uptime of the machine.

What is the Impact of Fixed Costs on Business Profitability?

All views and/or recommendations are those of the concerned author personally and made purely for information purposes. Nothing contained in the articles should be construed as business, legal, tax, accounting, investment or other advice or as an advertisement or promotion of any project or developer or locality. The reason is that the balance of unabsorbed / overabsorbed overhead must not be carried over from one year to another.

Unlike variable costs, fixed costs are not dependent on the production or output of goods or services. Moreover, fix costs often relate to time period, and generally do not change over time. Fixed overhead costs are costs incurred over time and tend to be unaffected by fluctuations in activity levels within a certain range. These costs are fixed in total as the output or production activity increases or decreases over a period of time. Fixed overhead per unit decreases as production increases and increases as production decreases. To calculate the total manufacturing overhead cost, we need to sum up all the indirect costs involved.

In such cases, management needs to see if production in the second shift can withstand such rising production costs. The costs incurred for additional activities or alternative courses are easily available after classifying the costs into fixed and variable costs. (also known as mixed or semi-fixed costs) are costs that include both fixed and variable factors and are therefore partially affected by fluctuations in activity levels. For example, telephone charges include a fixed portion of the annual charge and variable charges depending on the call, so the total telephone charges are semi-variable. However, to minimize fixed costs per unit, it is desirable to make the most effective use of plant capacity. Indirect labor is the cost to the company for employees who aren’t directly involved in the production of the product.

The Break-even point is the point where your total expenses match the total revenue, a point without any profit or loss, i.e. break-even. To put it in layman’s terms, the point where you finally recover all the capital costs borne to set up the business. The basic formula for break-even analysis is derived by dividing the total fixed costs of production by the contribution per unit . Capital expenditures are not recorded in profit-and-loss accounts, they are directly registered in the balance sheet and wear off slowly over time. Whereas, All the expenses are charged off against the company’s income in the same year they are incurred.

Applying the break-even analysis

Then the percentage of factory costs to direct wages is 50. Factory costs for the following year will be recorded at 50% of direct wages. The apportionment of overhead expenses is done by adopting suitable basis such as output, materials, prime cost, labour hours, machine hours etc.

The cost per unit of production decreases as the production volume decreases, but gradually increases as the production volume increases. For all productions, variable spending per unit of production is constant. Fixed overhead costs are not always completely fixed in nature.

Is depreciation a fixed asset?

Depreciation represents the periodic, scheduled conversion of a fixed asset into an expense as fixed asset is used during normal business transactions. Since the asset is part of normal business operations, depreciation is considered as revenue expense.

It helps them to decide the viability of a business idea, along with formulating pricing strategies and costs. There are more than a few ways to calculate your break-even point. The depreciation of assets also aids the business in forecasting cash requirements and determining when the likely cash outflow will occur. That is why using these two accounting concepts is crucial and paramount. Depreciation and amortization are two terms that are frequently used interchangeably, but they are governed by different accounting standards. The goal of depreciation is to spread an asset’s cost out over its useful life, whereas the goal of amortization is to capitalize an asset’s cost over its useful life.

Depreciation expense is estimated based mostly on precise cost and the estimated helpful life of an asset. The authentic cost of the asset doesn’t change over the life of its use within the business. Managing the fixed cost helps in optimizing the business financial structure, thereby making an apprised depreciation fixed or variable decision regarding pricing structure, business finances, and volume of product. Analysing the fixed cost of a business helps accountants draft the financial report and present it to business stakeholders. It also helps them perform computations and assess business’s financial stability.

Business Plan

Some fixed costs such as investments in infrastructure can not be substantially decreased in a limited time span are referred as fixed committed costs. While discretionary fixed costs depend on management decisions. The Units of Production technique is an exception to this rule. According to this method, the greater the number of units produced by your company , the greater your depreciation expenditure. As a result, when employing the Units of Production approach, depreciation expenditure is considered a variable cost.

There are several methods for calculating depreciation, including straight line, reducing balance, and annuity. Amortization can be calculated using a variety of methods, including Straight Line, Reducing Balance, Annuity, Bullet, and so on. Depreciation is a type of accelerated depreciation that shows how the value of a fixed asset depreciates as it is used. An office building, for example, can be used for several years before becoming run down and being sold. The cost of the building is spread out over the structure’s expected life, with a portion of the cost being expensed in each accounting year.

Why is depreciation a fixed asset?

Depreciation of fixed assets is an accounting term that is used to represent how much of an asset's value has been used up over time. Depreciation is, therefore, a calculated expense, which leads to a decrease in earnings.

The cost of large tools is generally capitalized and the appropriate depreciation costs are capitalized as factory overhead. Small tools are machinery and equipment used in the workplace. The cost of small tools is usually charged to all departments based on the actual problem. Using depreciation expense helps firms higher match asset makes use of with the advantages supplied by an asset. Why would a business willingly choose costlier early expenses on the asset?

What are variable costs?

The calculation on this instance is ($50,000 – $10,000) / 10, which is $four,000 of depreciation expense per yr. If a company buys a chunk of kit for $50,000, it might expense the whole price of the asset in yr one or write the value of the asset off over the asset’s 10-year useful life. Most enterprise house owners favor to expense only a portion of the cost, which boosts net revenue. As said earlier, carrying value is the web of the asset account and amassed depreciation. However, revenues could also be impacted by larger costs related to asset maintenance and repairs. To calculate depreciation expense, use double the straight-line price.

It is used for analysis under various disciplines like Biology, Economics, Maths, etc. You may need to sell a lot more products to achieve break-even, it is a good time to analyse the situation in a holistic approach. Some partial amortization loans have a balloon payment after the initial deferment or interest-only period.

For stocks that fluctuate significantly, it is important to include interest as the amount of capital required to maintain them varies. Replacement of existing machines with new ones are not appropriate without due consideration of profits. Through the ispatguru.com website I share my knowledge and experience gained through my association with the steel industry for over 54 years. Our company has team of Proficient Professional who are committed to provide the best quality services in hassle-free manner to clients.

Is depreciation a fixed or variable cost?

Depreciation is one common fixed cost that is recorded as an indirect expense.

The prices of X and Y are Rs 4 per unit and Rs 5 per unit respectively. Margin of safety is the extent by which actual or projected sales can exceed the break-even sales. It represents the amount gained or lost which defines how far or near the break-even point is.

In this way, variable costs fluctuate in direct proportion to total production, but tend to remain constant per unit even if production activity changes. Examples include indirect materials, indirect labor, corruption, tools, defective work losses, lubricants, idle time, lighting and heating costs, and sales commissions. Manufacturing overhead cost is the sum of all the indirect costs which are incurred while manufacturing a product. It is added to the cost of the final product along with the direct material and direct labor costs. Usually manufacturing overhead costs include depreciation of equipment, salary and wages paid to factory personnel and electricity used to operate the equipment. Every business needs to recover both of these costs since both costs are expenses of business.

Similar results can be obtained by arranging the data in ascending and descending order and comparing any set of two consecutive numbers. If concerns increase its capacity, additional equipment and buildings will need to be introduced and more staff will need to be appointed to meet the changed production requirements. If it is based on production volume, it will be part of the manufacturing cost as a direct cost, and if it is based on sales, it will be part of the selling cost.

A predetermined percentage of depreciation is attributed to the declining or written-off value of assets kept in the books at the beginning of a financial year instead of the asset’s purchase price. The annual depreciation and holding value of an asset decrease over time when using the lowering balance or shrinking balance technique. The straight-line approach is a simple way to calculate depreciation.

In this method, the output at two different levels, high or low, is compared to the amount of cost incurred during these different periods. Since fixed overhead costs are fixed, the ratio of variable overhead costs is the change in cost divided by the change in output level. One of the most important items influencing the profitability of farming operations is the cost of owning and operating the farm machines. Accurate cost estimates play an important role in every machinery management decision, namely, when to trade, which size to buy, how much to buy, etc. Fixed costs depend on how long a machine is owned rather than how much it is used. It includes depreciation, interest, taxes, shelter and insurance.

Such costs are incurred in the process of moving materials and goods from one location to another. A) Insurance for plants and machinery, buildings and equipment should be allocated to specific departments or cost centers as overhead items. Such costs should be allocated to the production sector according to the horsepower of the installed machine. Maintenance and repair costs are easy to find if done by an outside company, but in many cases large manufacturers have their own repair and maintenance departments. In order to confirm the amount in such a case, it is necessary to open an account individually with the identification number of the series called „service order“ for each repair work undertaken. The analysis of break-even points is very important for start-ups.

Is depreciation a fixed or variable cost?

Depreciation is one common fixed cost that is recorded as an indirect expense.

SKLADOVACÍ HALA

včetně školícího střediska